Last year, the Reserve Bank of India (RBI) released the Guidance Note on Operational Risk Management and Operational Resilience on April 30, 2024. This comprehensive document supersedes the earlier 2005 guidelines, reflecting the evolving nature of operational risks for modern digital banks.

This updated guidance aligns closely with the Basel Committee on Banking Supervision (BCBS)'s Principles for Operational Resilience, published in March 2021.

The new guidance document highlights the necessity for “regulated entities” to manage operational risks and build resilience against them. On reading the report, its evident that a key aspect of this resilience is observability—the ability to monitor, detect, and respond to issues in real-time across complex, interconnected systems. As banks integrate advanced technologies and expand their digital footprints, observability becomes important in ensuring uninterrupted service delivery and compliance with regulatory expectations.

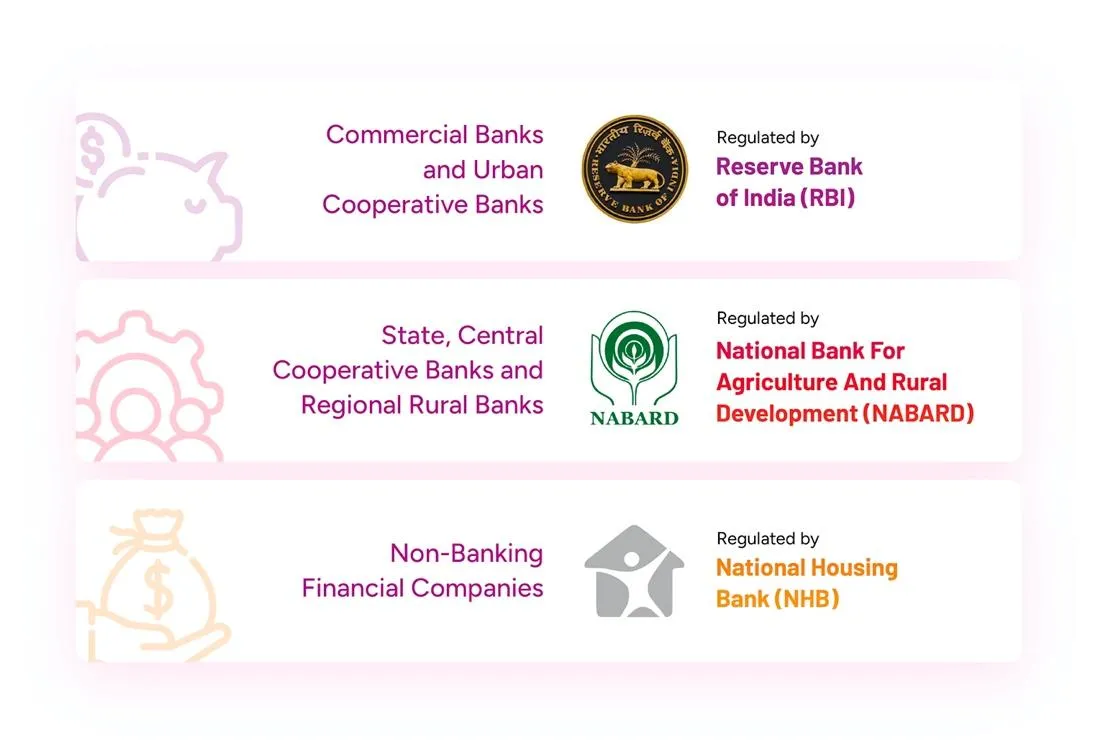

As highlighted earlier, the RBI Guidance document is applicable to “Regulated Entities”. These entities include

1. Commercial Banks

2. Co-operative Banks (Central, State, Urban)

3. Financial Institutions (ex: Exim Bank, NABARD, NHB, SIDBI, and NaBFID)

4. NBFCs

Fig 1: Supervisory Authority for each “Regulated Entities”

Understanding the Responsibilities of the Board of Directors, Senior Management, and Business Units from an Operational Resilience Standpoint.

The report highlights three lines of defense when it comes to adherence to Operational Risk.

The Business Units become the first line of defense and have the inherent responsibility to identify and mitigate systemic risks that can happen within banks' products or services. More importantly, the board plays the critical role of the third line of defense that independently reviews and allocates appropriate resources so that critical systems are equipped for success.

In the table below, we highlight the key responsibilities of each role when it comes to Operational Resilience

The Imperative of Observability in Operational Resilience

In the wake of the COVID-19 pandemic, the banking sector in India has undergone a significant digital transformation. The accelerated shift towards digital banking services has led to increased reliance on third-party providers, including fintech companies, cloud service providers, and API-based integrations. This interconnected ecosystem, while offering enhanced services and operational efficiencies, has also introduced new vulnerabilities and complexities in managing operational risks. The report acknowledges this development and highlights a few concerns from the perspective of reliability.

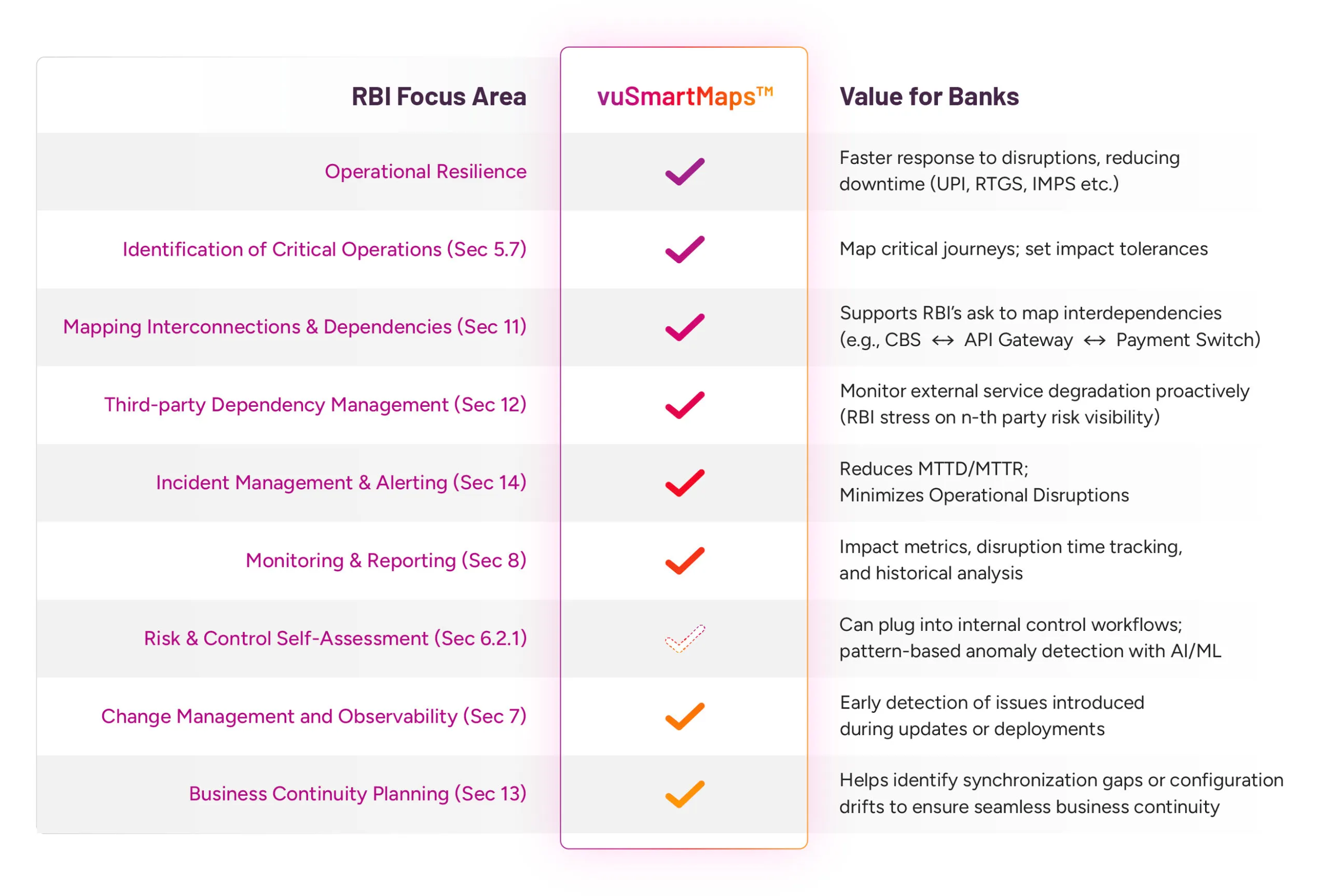

Key Observability Components Highlighted by RBI

- Comprehensive Mapping of Interconnections and Interdependencies: Identifying and documenting the intricate web of internal and external interconnections that support critical operations. This mapping facilitates a holistic understanding of potential vulnerabilities

- Establishment of Impact Tolerance Metrics: Banks must define clear impact tolerance levels for their critical operations. These metrics, which can be time-based, volume-based, or service-level-based, quantify the maximum acceptable level of disruption. Such quantification aids in setting thresholds for monitoring systems to trigger alerts when tolerances are breached.

- Integration of Incident Management with Monitoring Systems: The guidance emphasizes the need for robust incident management frameworks that are tightly integrated with observability tools. This integration ensures swift detection, classification, and response to incidents, minimizing potential impacts on operations.

- Continuous Monitoring and Feedback Loops: Institutions are encouraged to implement continuous monitoring mechanisms that not only detect anomalies but also facilitate feedback loops. These loops enable organizations to learn from past incidents, adapt their strategies, and enhance their resilience over time.

- Third-Party Dependency Monitoring: Given the reliance on third-party service providers, banks must monitor the performance and resilience of these external entities.

How vuSmartMaps™ Can Help Banks Stay Ahead?

Embracing Operational Resilience in 2025

The RBI guidance note on Operational Risk Management and Operational Resilience is a necessary focus in the regulatory landscape, acknowledging the dynamic transformation in the past few years. As digital banking ecosystems become increasingly interconnected, end-to-end visibility into critical systems becomes non-negotiable.

We like to believe that platforms like vuSmartMaps™ play a crucial role in this transformation. The focus on real-time monitoring, incident management, and third-party dependency tracking helps banks proactively address disruptions, maintain service continuity and uphold customer trust.

As the financial sector continues to evolve, embracing such advanced observability solutions will be instrumental in achieving operational resilience, ensuring compliance, and fostering a robust, customer-centric banking environment.